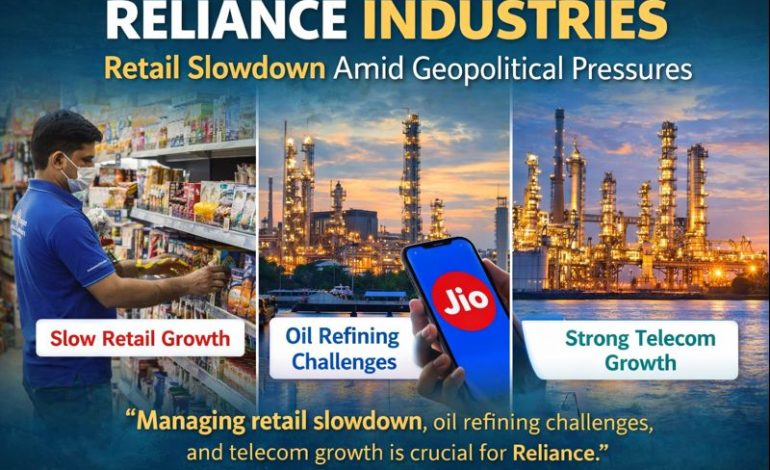

Reliance Industries, India’s largest conglomerate, is navigating a complex landscape of geopolitical tensions and domestic business challenges. While the company has managed to maintain steady growth in its oil refining and telecom sectors, its retail business—the group’s third-largest segment—has emerged as a key concern for analysts and investors.

Retail Slowdown Raises Concerns

Reliance Retail’s revenue grew just 8.1% year-on-year, while its EBITDA increased only 2% in the December quarter. This slower growth has prompted brokerages such as Citi and UBS to revise down their target prices for Reliance shares, though they continue to maintain buy ratings.

Isha Ambani, head of Reliance Retail, remains optimistic, stating, “We are confident of delivering 20%+ CAGR in retail revenues over the next three years.”

However, Macquarie Capital removed Reliance from its Asia Marquee list, noting that Reliance Retail’s performance is a key factor in the group’s overall valuation.

Brokerage Revisions and Market Impact

-

Citi lowered its target price from 1,860 rupees ($19.9) to 1,815 rupees per share.

-

UBS reduced its target from 1,820 rupees to 1,790 rupees, citing slower-than-expected retail growth.

The December quarter saw mixed consumer demand. Sales of gold and automobiles rose, while fashion and consumer staples reported softer growth. Bernstein analysts warned of a gradual recovery in 2026, with limited short-term catalysts for consumer demand.

Industry-Wide Retail Trends

Reliance Retail’s peers, including Avenue Supermarkets and Tata Group’s Trent, also reported slower growth in the December quarter. The company highlighted that consumer staples were demerged during the period, now operating as a direct subsidiary, accounting for roughly 5% of total revenue.

Brokerages view the slowdown not as a temporary blip, but as part of a secular downtrend. Citi revised Reliance’s consolidated EBITDA forecasts for FY2026–28 downward by 1–2%, reflecting the moderation in retail growth.

Oil-to-Chemicals Business Navigates Geopolitical Tensions

Reliance had to cut imports of cheap Russian crude due to U.S. sanctions on Rosneft and Lukoil. At its peak, Russian oil made up 40–45% of Reliance’s crude mix, according to Pankaj Srivastava of Rystad Energy.

Despite these challenges, EBITDA for the oil-to-chemicals segment rose 15% year-on-year, as strong refining margins offset lower Russian crude intake, higher freight costs, and weak petrochemical demand, according to Goldman Sachs.

New Energy Ventures and Battery Storage Plans

Geopolitical factors reportedly impacted Reliance’s new energy projects, including a 40-gigawatt battery storage plant. Bloomberg reported delays due to technology transfer restrictions from China.

The company, however, denied delays. Karan Suri, senior VP of new energy, confirmed that construction is progressing and commissioning will occur in the next few quarters.

Telecom Business Continues Steady Growth

Untouched by retail challenges or geopolitical issues, Reliance’s telecom arm continued to deliver strong results, reporting:

-

12.7% year-on-year revenue growth

-

16.4% increase in EBITDA

-

8.9 million new customers, raising total subscribers to 515 million

The telecom business is also preparing for a planned listing this year, which is expected to further strengthen the group’s financial position.

Conclusion

While Reliance Industries continues to weather geopolitical headwinds and maintain performance in its oil and telecom segments, the slowdown in Reliance Retail remains the primary domestic challenge. Strategic focus on infrastructure, value addition, and consumer engagement will be key to sustaining growth and restoring investor confidence in India’s largest conglomerate.